Where to now? Banks, Fed, Markets...

My brother and I often joke that we will rest in the coming "lull"

The "lull" never comes.

This is much like the recent "lull" between Q4 earnings reported in Jan/Feb and Q1 earnings which start to come out in April.

With SVB, Silvergate and more banks failing, the "lull" was anything but!

Investor focus turned to inflation and the Fed, and we were dealt a twist in the form of SVB (Silicon Valley Bank's failure) and it's implications for regional banks as a whole.

Today I cover:

Fed Raise: More "under the hood" of 25bps

SVB: Was it a "blip" or sea change in risk?

Markets - where do we go from here?

Fed Raise: More "under the hood" of 25bps

First, Powell had every excuse NOT to raise, and he did.

That shows you how committed he is to the path. What path? Getting rid of the Fed Put. The Fed Put is the idea that anytime markets go down, the Fed will back off to support markets. The Fed Put says that in a game of chicken, the Fed will always lose so markets don't have to.

The Fed Put creates a big problem:

Markets don't function if you think you can't lose.

As Danielle DiMartino Booth so eloquently wrote in a longer piece this week (worth reading as she lowered the paywall for this piece), Powell tried this early in his tenure to kill the Fed Put, but didn't have the political power to stay the course. Regulators, including the Fed, have far more latitude when things are already falling apart.

How do you get rid of the "idea" that you will come to the rescue?

Just like a parent, you let everything fall apart. Enough that it hurts. We are not there yet. If we were, semiconductor stocks wouldn't have rallied 25% in the first 3 months of 2023. Investors have not capitulated (enough). The Fed needs capitulation to get rid of the Fed put.

I can hear some friends saying: "well, Emmy, its only 25bps".

(1) The ABSOLUTE level of 5% matters. Especially in an economy built on 1% or less interest rates. (2) Powell said he will work on shrinking the Fed's balance sheet. These actions make credit tighter.

From the (horse's mouth), aka Fed Meeting:

“Recent developments are likely to result in tighter credit conditions for households and businesses and to weigh on economic activity, hiring, and inflation,” the Federal Open Market Committee (FOMC)

In other words, the odds of getting turned down for a loan may have gone up by an uncertain amount as banks assess the

“Such a tightening in financial conditions would work in the same direction as rate tightening,” Fed Chair Jerome Powell explained during

Summary: Economies grow on expanding credit, but we can't expand forever (it's just math), otherwise our economy gets overheated (inflation). We are in the midst of a reset. Powell now has the political will and ability to do what he says. He's getting rid of the Fed Put.

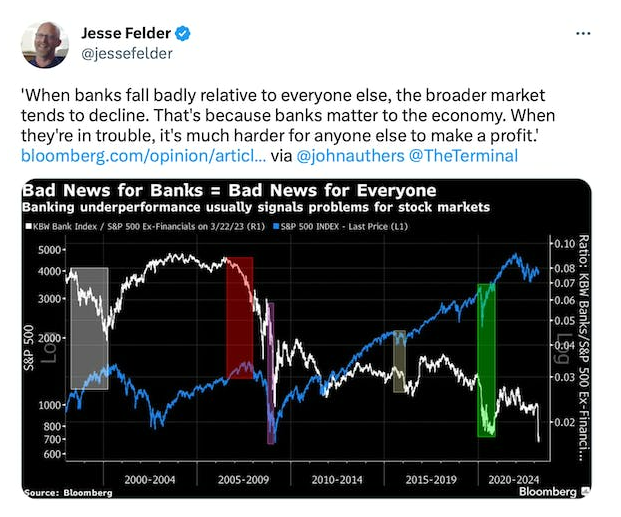

SVB: Blip, one off, or sea change?

Some in Silicon Valley are breathing a sigh of relief, saying that was just a blip. Others are saying this was a risk-off sea change wake up call.

Go back to what you and I, people on the street, know. What do you hear?

When I look on Twitter, I see every company, even ones taking deposits back to SVB, say they will always have two bank accounts from here on out. The second bank account is with a big-4 too big to fail, quasi government guaranteed bank

If every company that is a regional bank customer now splits their deposits between a regional and mega bank...all those uninsured deposits move to the mega banks... Then regional banks continue to see a slow run on their banks, like a slow moving train crash.

Regional banks are way over-indexed to commercial real estate loans. Those commercial real estate loans are symptoms of banks going out on the risk curve to chase yield. These are cracks that appear when rates rise and the economy slows.

Want to dive deeper into the banking and credit crunch?

Read John Hussman's latest piece. He argues that the failure did not occur because there is too little liquidity in the banking system as a whole. It occurred because there is too much. Hit the link to read his full piece...

Markets - Where now?

Q1 earnings are up next. Powell is steadfast in wanting to remove any idea that the Fed will come to investors' rescue. And we likely haven't heard the last of the banking crisis.

Meanwhile, we had a nice rally off the end of December lows.

As a reminder, Bear Market Rallies can range from 20-50%, and then the market can move lower still.

Hussman, while he makes no forecasts, says we are in a period he calls a "trap door" or the edge of the edge:

Investors are on-edge, more risk averse, after seeing several runs on banks and some lost equity/bond valuations in those banks.

Tech investors have crowded into "safe" names like AAPL and MSFT, which now make up 13.3% of NASDAQ. This is the definition of a narrow, highly risky market situation.

Now we head into Q1 earnings season. Q1 is typically seasonally slow for most businesses. It might be tough to differentiate between cyclical or seasonal slowing, but Q1 is not where we will see "upside".

A bit more on crowding into "safe" names. We investors have seen this movie before. It goes like this:

Sell risky stocks, those you "took a flyer on" first

Keep your market exposure the same by buying more large stocks

Your safe bets miss earnings. You give up entirely, selling it all.

Added together, this is the playbook for a trap door followed by a big gap down in markets. Bears need these to wash out the rest of the speculators and reach true capitulation.

History rhymes

The same thing happened in 2007, when banks became the largest portion of the S&P500 than they had been in decades. I shorted them just off that fact alone. Now that is the case for large cap tech (still, even with all the declines in tech names).

Silver Lining

With every quarter that passes, we trudge through the economic slowdown, perhaps still on the down slope, but further through it.

With every quarter that passes, we are also digesting worse earnings, slower growth, and therefore CREATING EASIER COMPS!

So with every quarter that passes, we should be sharpening our pencils, finding great ideas, but being patient enough to wait until the time is right to invest in them.

I am taking a look now at the amazing innovation that GPT-4 will create, in itself, and even more for software, identity and services businesses that either leverage it or protect against the risks it creates.

Happy Hunting!